Demand for critical minerals – essential for high tech, energy and defence applications – is high, yet production is concentrated in a limited number of countries, leaving supply chains vulnerable to disruption and price volatility. Recent geopolitical developments, including the Iran conflict and Chinese export restrictions, have underscored these risks and the strategic importance of diversifying supply. In response, governments are stepping up policy and financial support for critical minerals investment, recognising that market economics often render these capital-intensive projects unviable without public intervention.

In this briefing, we explore the different government policies and initiatives for financing critical minerals projects in key jurisdictions.

Key takeaways:

- Demand for critical minerals is rising, but supply remains concentrated, making markets vulnerable to disruption while investment in new projects has slowed.

- Governments are increasingly taking the lead with funding, equity, guarantees and long-term offtake arrangements to make projects commercially viable.

- Major economies are combining domestic measures with international partnerships to secure more reliable and diversified critical mineral supply chains.

Concentration of global supply chains

According to the International Energy Agency’s (IEA) 2025 Global Critical Minerals Outlook, “the average market share of the top three refining nations of key energy minerals rose from around 82% in 2020 to 86% in 2024 as some 90% of supply growth came from the top single supplier alone: Indonesia for nickel and China for cobalt, graphite and rare earths.”

This concentration has resulted in significant uncertainty and risk for investors, in particular exposure to supply shocks. In parallel, while some countries in the Middle East have expanded their role in downstream processing of critical minerals in recent years, processing capabilities remain geographically concentrated and closely tied to regional energy and logistics stability.

Aluminium – a highly energy-intensive and geopolitically exposed input critical to defence, electric vehicles, renewable energy infrastructure and grid systems – is a particular pressure point, prompting governments to prioritise domestic smelting capacity, recycling and supply chain security alongside broader critical minerals strategies.

Despite strong demand, investment into critical minerals projects has waned in recent years, which only exacerbates the concentration of supplies from a limited number of countries. This in turn increases the risk of price fluctuations and supply disruptions. The IEA reports: “Investment momentum in critical mineral development weakened in 2024, with spending rising by just 5%, down from 14% in 2023. Adjusted for cost inflation, real investment growth was just 2%.”

How certain jurisdictions are providing support to investors

Highly concentrated supply chains have created an environment for government support for new investments in critical minerals to diversify supply chains. “Critical minerals policy has moved beyond industrial strategy and is a matter of economic security. Governments are no longer acting solely as regulators of mining projects; they are becoming active participants in project risk allocation, financing structures and supply chain outcomes,” says Brett Cohen, a Clifford Chance Partner based in Perth. Many jurisdictions around the world have implemented or announced policies in connection with financing and supporting the development of critical minerals projects.

United States

Since 2017, the US has developed an increasingly co-ordinated federal policy framework to support the development of domestic and international critical mineral and rare earth element projects to reduce reliance on foreign supply chains. Federal support has taken the form of executive action, trade policies and tariffs, several different pieces of legislation, multiple government financing, funding and support programs, direct procurement, equity investments, tax incentives and less environmental scrutiny.

Through a series of executive orders, both the Trump and Biden Administrations emphasised the strategic importance of critical minerals to defence, semiconductor manufacturing, advanced technologies and broader industrial competitiveness, and have directed federal agencies to use the tools available to them to support projects spanning extraction, processing, refining and manufacturing. Multiple agencies across the federal government are supporting both domestic and international projects using all of the policy tools mentioned above. These agencies include the Department of War (DoW), the Department of Commerce (DOC), the Department of Energy (DOE), the EXIM Bank (EXIM) and the US International Development Finance Corporation (DFC). Examples of recent US federal agency transactions and announcements include:

- MP Materials: DoW made a US$400 million equity investment into MP Materials, (a US critical minerals company, specialising in rare earths), issued a US$150 million loan from its Office of Strategic Capital, established a price floor for Neodymium-Praseodymium product – a rare earth which is used for defence systems, robotics and advanced electronics – and entered into a 10-year magnet offtake agreement.

- Korea Zinc Crucible Metals: DoW and DOC entered into a strategic partnership with Korea Zinc to build a US$7.4 billion critical minerals smelter in the US. DoW, together with private investors, will invest approximately US$2.15 billion in Korea Zinc, DoW will provide separate debt financing from its Office of Strategic Capital, and DOC will provide US$210 million in award funding under the CHIPS and Science Act 2022 (and receive equity).

- Project Vault: Through a public-private partnership funded with a US$10 billion loan from EXIM and US$2 billion in private sector investment, EXIM will establish a U.S. Strategic Critical Minerals Reserve, a stockpile of critical minerals designed to protect the private sector from supply chain disruptions, price volatility and market manipulation. Project Vault would require private companies to commit to purchase certain minerals at a fixed price and pay storage costs and fees.

- DOE Grants: Different offices within DOE have approximately US$1 billion in funding available to award to companies to advance and scale mining, processing and manufacturing technologies including, for example, start-up companies developing next-generation mining, recovery and processing technologies.

- Serra Verde: DFC issued a US$565 million loan to optimise and expand the Pela Ema rare earths mine in Brazil, owned by Serra Verde, to help develop a Western aligned source of rare earth elements, including heavy rare earth elements. In addition, Serra Verde has secured a 15-year offtake agreement with a special purpose vehicle funded by US federal agencies and the private sector that includes commodity price floors.

Companies developing critical minerals projects in the US may also be able to take advantage of the 45X Advanced Manufacturing Production Tax Credit (a 10% credit on production costs for over 50 domestically produced or refined critical minerals) and the 48C Advanced Energy Project Investment Tax Credit (a credit of up to 30% of investment costs for projects that re-equip, expand or establish industrial facilities for the processing, refining or recycling of critical minerals).

Importantly, the United States has not confined its support solely to domestic projects. Rather, it is increasingly using EXIM, DFC and allied-country co-ordination to support overseas projects that contribute to diversified, geopolitically resilient supply chains aligned with US strategic objectives.

This outward-looking strategy reflects a recognition that US domestic production alone will not be sufficient to meet future demand and that supply chain resilience requires diversified sources across trusted jurisdictions.

Complementing its unilateral measures, the US has pursued an expanding network of bilateral and multilateral partnerships designed to align critical-minerals policies with key allies. These include:

- participation in the Minerals Security Partnership (MSP) alongside countries such as Australia, Canada, Japan, the EU and the UK, aimed at co-ordinating project finance, standards and supply chain development;

- bilateral critical minerals agreements and cooperation frameworks with Australia, Japan and the EU, enabling shared access to investment incentives, tax credit eligibility and project level collaboration; and

- the United States – Japan Framework, entered into in October 2025, to boost funding and accelerate permitting for eligible projects.

“The United States has built a robust federal regime increasingly co-ordinated with the private sector to secure critical mineral supply chains, combining direct investment, long-term offtake, tax incentives, access to federal land and research and development funding across the full value chain,” says Peter Hughes, a Clifford Chance Partner based in Washington, DC.

European Union

The EU’s response has been to treat critical minerals not merely as a trade issue but as a core element of economic security, industrial policy and strategic autonomy. It has adopted a variety of regulatory and support measures, including:

The Critical Raw Materials Act

The Critical Raw Materials Act (CRMA), which entered into force in 2024, provides the central legal framework for EU action. It sets quantitative targets for 2030 for strategic raw materials across the value chain, including:

- at least 10% of annual EU consumption from domestic extraction;

- 40% from processing within the EU;

- 25% from recycling; and

- a cap of 65% dependency on any single third country for each strategic raw material.

The CRMA explicitly aims to improve the bankability of projects by designating “Strategic Projects”. By early 2026, the European Commission had identified 47 strategic critical minerals projects across mining, processing and recycling, signalling political backing and priority treatment in administrative procedures.

In addition, the European Commission has announced that it will introduce, in early 2026, restrictions on the export of scrap from and the waste of permanent magnets, as well as targeted measures on aluminium scrap. Similar actions will be considered for copper scrap if this proves necessary. This would also support European recycling capabilities.

Financial support and public finance instruments

Recognising that critical minerals projects are capital-intensive, long-term and exposed to commodity price risk, the EU has moved decisively to deploy public f inance as a catalyst.

Under the RESourceEU Action Plan, adopted in December 2025, the European Commission committed to mobilising up to €3 billion in EU funding over a 12-month period to, inter alia, de-risk strategic critical minerals projects and secure alternative supplies in the short term.

A key institutional innovation is the planned European Critical Raw Materials Centre, expected to become operational later in 2026. The Centre is intended to provide market intelligence, steer and finance strategic projects using tailored instruments with private and public partners, and act as portfolio manager for diversified and resilient supply chains, including through joint purchasing and stockpiling.

The European Investment Bank (EIB) has significantly expanded its role in critical minerals financing. In March 2025, the EIB adopted a Critical Raw Materials Strategic Initiative, aligning its lending and advisory activities with the CRMA and allowing f inancing across the entire value chain, both within and outside the EU.

Promotional banks at national level also provide funding to improve the availability of critical raw materials. For example, in 2024 the German government set up a “Raw Materials Fund” (Rohstofffonds). The Fund targets projects along the entire raw materials value chain both within Germany/EU and in third countries provided that they secure long-term offtake for Germany or the EU and thus contribute to safeguarding raw material supply security and Germany’s – and the EU’s – strategic autonomy in line with the CRMA.

Strategic Partnerships and the Global Gateway

The EU recognises that domestic extraction alone will not meet future demand. As a result, external action is a core pillar of its strategy. Through Strategic Partnerships on Raw Materials, the EU has concluded (legally non-binding) memoranda of understanding with resource-rich countries including Canada, Australia, Chile, Argentina, Namibia, Kazakhstan, Ukraine, Rwanda and Greenland, among others.

In April 2026, the EU and the US signed a Memorandum of Understanding for a strategic partnership on critical minerals, agreeing an EU-US Critical Minerals Action Plan to coordinate trade policies and measures on critical minerals supply chains.

These arrangements focus on cooperation across the full value chain such as mining, processing, recycling, ESG standards and skills development, and are closely linked to the EU’s Global Gateway initiative. The emphasis is on mutually beneficial, rules-based and diversified supply chains, supported by EU and national public-finance institutions.

“The EU has elevated critical minerals to a central pillar of economic security, using the Critical Raw Materials Act, targeted public finance and strategic partnerships to actively shape resilient, diversified supply chains rather than leaving outcomes to the market alone,” says Thomas Voland, a Clifford Chance Partner based in Düsseldorf.

United Kingdom

In late 2025, the UK government published its updated Critical Minerals Strategy, setting out a framework for supply chain resilience, international partnerships and selective domestic capability building. The Department for Business and Trade will make “up to £50 million” available to support critical mineral projects, including their research, innovation and commercialisation. The detailed structure and eligibility criteria are being developed, with further details expected later in 2026.

UK Export Finance (UKEF) is supporting supply chains through Critical Minerals Supply Finance, which backs overseas projects linked to UK supply arrangements, and a Critical Goods Export Development Guarantee, which provides guarantees to lenders supporting UK-based suppliers. Both schemes require a clear UK supply chain or export nexus. The National Wealth Fund has also shown a willingness to support the critical minerals sector through recent investments in a UK-based lithium project.

The British Industry Supercharger, introduced in April 2024, provides electricity-cost relief for qualifying energy-intensive industries, including the processing of many critical minerals, with additional network charge relief expected from April 2026. The government has also consulted on a proposed British Industrial Competitiveness Scheme, which is expected to reduce electricity costs more broadly for qualifying businesses from 2027.

In January 2026, Japan and the UK renewed their partnership with a focus on strengthening cooperation around critical mineral supply chains. This renewed collaboration aims to ensure that both countries have access to reliable, transparent and sustainable sources of essential minerals, which are vital for advanced manufacturing, green technologies and the energy transition. The partnership is expected to involve joint initiatives to diversify supply sources, promote responsible sourcing practices and encourage innovation in mineral processing and recycling.

By working together, Japan and the UK seek to reduce dependency on single suppliers and mitigate risks associated with geopolitical tensions or market disruptions. The partnership also underscores a shared commitment to high environmental and social standards in the extraction of and trade in critical minerals, supporting broader goals of sustainability and resilience in global supply chains.

“The UK’s updated Critical Minerals Strategy reflects a pragmatic shift toward supply chain resilience – pairing targeted public funding, export-linked finance and industrial power-cost relief to support strategically important projects while leveraging international partners, rather than pursuing wholesale domestic self sufficiency,” says Craig Nethercott, a Clifford Chance Partner based in London.

Japan

Following the enactment of the Economic Security Promotion Act in 2022, the Japanese government has deployed a “full-spectrum” strategy to further secure its critical mineral supply chains. The strategy combines offering substantial domestic subsidies, providing direct support for offshore investments made by Japanese companies and entering into strategic trade partnerships with key partners.

The Japan Organisation for Metals and Energy Security (JOGMEC) a limb of the Ministry of Economy, Trade and Industry, provides significant financial support to Japanese companies engaging in exploration, feasibility studies, mine development and refining processes for critical minerals, both domestically and abroad. JOGMEC offers funding support in the form of direct grants (covering up to 50% of the project costs for an eligible project), equity subscription, debt financing and guarantees for commercial loans. In particular, the direct grants offered by JOGMEC have been particularly successful, with six eligible projects being selected to date.

As part of its broader strategy to promote national and international critical mineral supply chain security, the Japanese government is actively transitioning from relying on simple bilateral mineral trade deals toward developing integrated, multilayered supply chain frameworks with like-minded trade partners (involving co-ordinated stockpiling, synchronised permitting and joint funding for mining and smelting projects). These frameworks prioritise a “right-shoring” approach that emphasises economic security, resilience and strategic autonomy over the reliance on specific trade relationships. As mentioned earlier in this article, most notably, (1) the Japanese government signed the Japan-U.S. Framework in October 2025 to facilitate funding and accelerate permitting of eligible projects, and (2) the Japanese and UK governments in January 2026 announced their renewed partnership to support collaboration on resilient, transparent and sustainable critical mineral supply chains.

In addition, the Japanese government is heavily investing in deep sea mining technologies to enable the extraction of rare earths sediments from the seafloor, in an effort to reduce import reliance. In February 2026, the Japanese government announced that a deep sea test in the Pacific Ocean had retrieved sediment containing rare earths from depths of 6,000 metres. Japan’s waters are estimated to contain over 16 million tonnes of rare earths, the third largest reserve globally, representing an enormous opportunity for Japan to become a key player in the extraction and exportation of these minerals. “Japan is pivoting from bilateral mineral trade toward state-supported, integrated critical mineral supply frameworks with trusted partners, focused on resilient supply chains and security of supply” says Hans Menski, a Clifford Chance Partner based in Tokyo.

Australia

The Australian Federal Government has recently introduced numerous incentives to promote the development of critical minerals domestically.

- In 2024, the Australian Government introduced a Critical Minerals Production Tax Incentive scheme to support the critical minerals industry and promote the downstream processing of critical minerals. This will provide a refundable tax credit on 10% of certain costs associated with the production and refining of critical minerals in Australia. The incentives, available for a period of 10 years for each project, are uncapped.

- The Australian Government has established a A$4 billion Critical Minerals Facility, which provides financing for critical mineral projects in Australia that are in Australia’s national interest. Export Finance Australia, which administers the facility, is collaborating with the Export-Import Bank of the United States to create a streamlined, single point of entry access for funding from both agencies. In late 2024, Australian mining company Iluka Resources secured a A$1.65 billion non-recourse loan from the Critical Minerals Facility for the development of the Eneabba rare earths refinery in Western Australia.

- In April 2025, Australia announced a Critical Minerals Strategic Reserve, which would give the Australian government the power to “purchase, own and sell critical minerals” and ensure Australia can “deal with trade and market disruptions from a position of strength”. The reserve, which has not been established as at the date of this article, would have two key features – (1) national offtake agreements under which the Australian government would acquire agreed volumes of critical minerals from commercial projects or establish an option to purchase at a given price, and (2) selective stockpiling under which the Australian government would establish stockpiles of certain key critical minerals produced under offtake agreements as required.

“Australia has moved decisively to position itself as a global critical minerals hub, combining long-dated, uncapped tax incentives, state-backed project finance and proposed sovereign offtake and stockpiling arrangements to crowd in private capital and support downstream processing at scale,” says Armin Fazely, a Clifford Chance Counsel based in Perth.

Deep sea mining

Deep sea mining is increasingly viewed as a potential answer to the rising demand for critical minerals required for the global energy transition. The sector offers opportunities to access untapped resources on the ocean floor, but these are fraught with legal, environmental and commercial uncertainties. The international regulatory landscape, particularly under the United Nations Convention on the Law of the Sea, remains in flux, with ongoing debates about the adequacy of environmental safeguards and the allocation of liability. These uncertainties pose significant challenges for investors and operators considering entry into the market.

In addition to regulatory hurdles, deep sea mining faces mounting scrutiny from environmental groups and other stakeholders concerned about the potential impact on marine ecosystems and biodiversity. The lack of established environmental standards and the risk of reputational damage further complicate project development and financing.

As the sector evolves, careful navigation of complex permitting regimes and stakeholder expectations will be essential. For further insights, see Clifford Chance’s recent briefing: The race to mine the seabed: opportunities and risks

The outlook for critical minerals

Demand for critical minerals is expected to continue to grow, given their importance to the modern world. The IEA has predicted that demand for lithium will grow fivefold by 2040, with demand for cobalt and rare earths rising 50-60% by 2040.

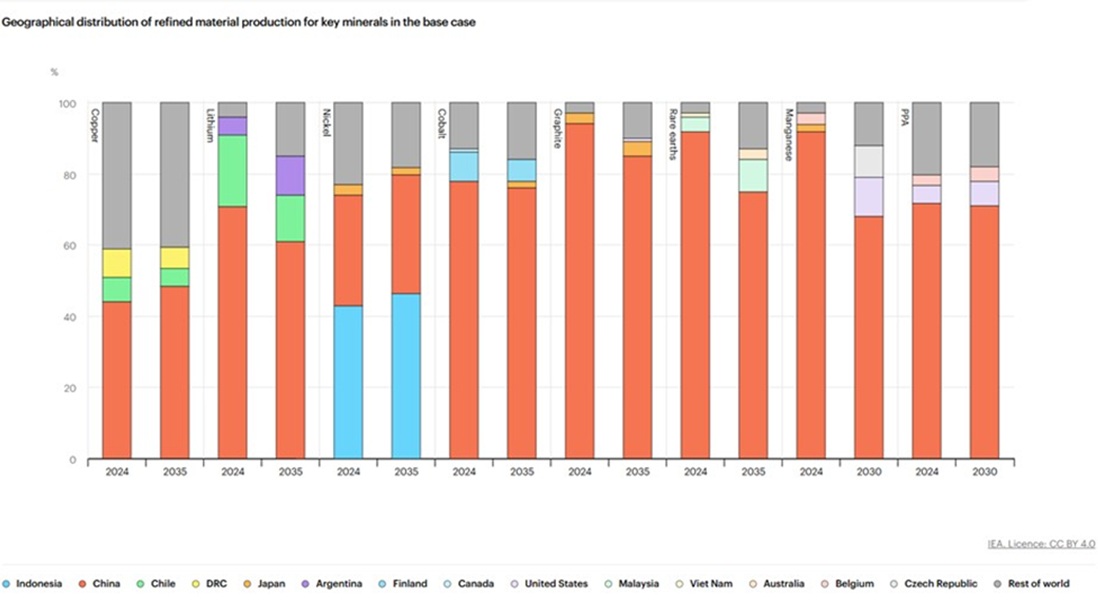

At the same time, the production of critical minerals is expected to remain highly concentrated over coming years. At the same time, the production of critical minerals is expected to remain highly concentrated over coming years, as illustrated by the following graph published by the IEA:

To meet growing demand, substantial investments will be required in new critical minerals projects. Challenges associated with developing mining projects persist, including the significant capital expenditure that is required, burdensome regulation and the need for long-term financing. Clifford Chance recently published a paper that considered some of these challenges: Energy transition perspectives: batteries, trade and critical minerals.

For all of these reasons, many see it as essential that governments set policies that promote and facilitate the development of critical minerals projects. If critical minerals supply chains are to become more balanced, that government support will be required to absorb the risks that the private sector has been unable – or unwilling – to absorb. “The imbalance between growing demand and concentrated supply means critical minerals projects will require governments to underwrite risks the market alone will not bear,” says Liz Humphry, a Clifford Chance Partner based in Perth.

Of course, changing government policies can also lead to risks, with the demand for critical minerals leading to a resurgence of resource nationalism in some parts of the world as producers of critical minerals seek to capitalise on demand for their natural resources. Investors should thus remain aware of and consider how to insulate their investments from sovereign risk, including by ensuring that their contracts incorporate adequate protections and by considering the availability of protection under international investment treaties. “These tools are invaluable to investors seeking to navigate a changing regulatory landscape in the critical minerals space and investors should be sure that they understand and use them to protect the value of their investments”, says Elliot Luke, a Clifford Chance Partner based in Perth.